Stripe is the name most businesses reach for first when they need to accept payments online. It’s reliable, developer-friendly, and powers millions of businesses. But it isn’t the right fit for everyone, and in 2026 the list of strong Stripe alternatives is longer than ever.

Some businesses want lower fees. Some need better support, local payment methods, or a merchant of record that handles tax. Others simply want to avoid the sudden fund holds Stripe is known for.

This article breaks down the best Stripe alternatives for 2026. It covers what each one does well, where it falls short, verified current pricing, and how each handles subscriptions. Putler appears at the end, not as a payment gateway, but as the tool that pulls all of them into one dashboard.

What is Stripe?

Stripe is an online payment processing platform that lets businesses accept card and digital payments over the internet. Founded in 2010, it became the default choice for startups and developers thanks to its clean APIs, strong documentation, and fast setup.

Stripe charges a flat 2.9% + $0.30 per successful online card transaction in the US, with no monthly or setup fees. That simplicity is the draw. You can start accepting payments within hours.

Under the hood, Stripe handles card processing, fraud screening, subscriptions, and payouts. It supports 135+ currencies and connects to almost every ecommerce platform and shopping cart on the market.

So if Stripe is this capable, why would you need an alternative? The answer comes down to fit.

Why do you need Stripe alternatives?

Stripe works well for a lot of businesses. It just doesn’t work best for all of them. Here are the most common reasons businesses look elsewhere in 2026.

Fund holds and account freezes: Stripe is a payment aggregator, which means thousands of businesses share underlying merchant accounts. When its risk systems flag unusual activity, they can freeze funds first and investigate later. For a small business, a sudden hold on payouts is a real cash-flow problem.

Flat-rate pricing stops scaling: the 2.9% + $0.30 rate is the same whether you process $1,000 or $1 million. Once you cross roughly $10,000 a month, interchange-plus processors often work out cheaper because they pass through the actual card-network cost plus a small markup.

No PayPal support: Stripe does not let you accept PayPal, since the two are direct competitors. If your customers expect a PayPal button, that’s a conversion problem.

High-risk restrictions: Stripe declines or limits certain industries. Businesses in those categories need a specialized high-risk merchant account.

No merchant-of-record option: Stripe is a payment gateway, not a merchant of record. You stay legally responsible for global sales tax, VAT, and compliance. For a SaaS company selling worldwide, that’s a growing burden.

Support that doesn’t scale with urgency: when payments break on a Friday afternoon, a ticket queue and a help-center article often aren’t enough.

Now let’s look at the best Stripe alternatives and how each one addresses these gaps.

Quick comparison of Stripe alternatives

Before the detailed breakdowns, here’s how the top Stripe alternatives compare at a glance. All pricing is verified as of 2026.

| Payment Gateway | Transaction Fee | Monthly Fee | Best For | Global Availability |

|---|---|---|---|---|

| Stripe | 2.9% + $0.30 | None | SaaS, developers, startups | 47+ countries |

| PayPal | 2.99% + $0.49 | None | Consumer trust, marketplaces | 200+ countries |

| Square | 2.9% + $0.30 online, 2.6% + $0.15 in-person | $0 (Plus $49) | Omnichannel and in-person retail | ~9 countries |

| Adyen | Interchange++ (~0.6% markup + $0.13) | ~$120 minimum | Enterprise, high-volume global | Global |

| Braintree | 2.59% + $0.49 | None | PayPal integration, enterprise | 45+ countries |

| Authorize.net | 2.9% + $0.30 | $25 | Established businesses, security | US, Canada, UK, Europe, Australia |

| Razorpay | 2% domestic (+18% GST) | None | Indian and Southeast Asian markets | India focused |

| 2Checkout (Verifone) | 3.5% + $0.30 to 6% + $0.50 | None | Global digital products, MoR | 200+ countries |

| Paddle | 5% + $0.50 | None | SaaS, merchant of record | Global |

Keep in mind that fees vary based on transaction volume, business type, and negotiated rates. Always check the latest pricing on each platform’s website before deciding. Now let’s explore each alternative in detail.

Best Stripe alternatives for eCommerce and SaaS

A reliable payment solution is critical for any online business. While Stripe is a popular choice, each of these alternatives offers something it doesn’t, whether that’s consumer trust, lower fees at scale, local payment methods, or merchant-of-record tax handling.

1. PayPal

PayPal is one of the most recognized and trusted payment platforms in the world, with over 430 million active accounts. It integrates easily with ecommerce sites and supports credit cards, debit cards, and the PayPal wallet, giving customers familiar options at checkout.

Pros

- Consumer trust: the PayPal button at checkout boosts buyer confidence and can lift conversion.

- Flexibility: a wide range of supported payment methods, including Pay in 3 and Venmo.

- Security: strong buyer and seller protection built in.

- Global reach: operates in 200+ countries, more than almost any competitor.

Cons

- Higher fees: the 49-cent fixed fee hurts on small transactions, and wallet payments run 3.49% + $0.49.

- Limited customization: the checkout experience is harder to tailor than Stripe’s.

- Strict policies: some industries face holds or restrictions.

Pricing

PayPal charges 2.99% + $0.49 for standard online card transactions, and 3.49% + $0.49 for PayPal wallet and Venmo payments. International transactions add roughly 1.5%. Check detailed pricing here.

If you’re running PayPal alongside other gateways, centralized PayPal analytics can help you track performance across every payment source.

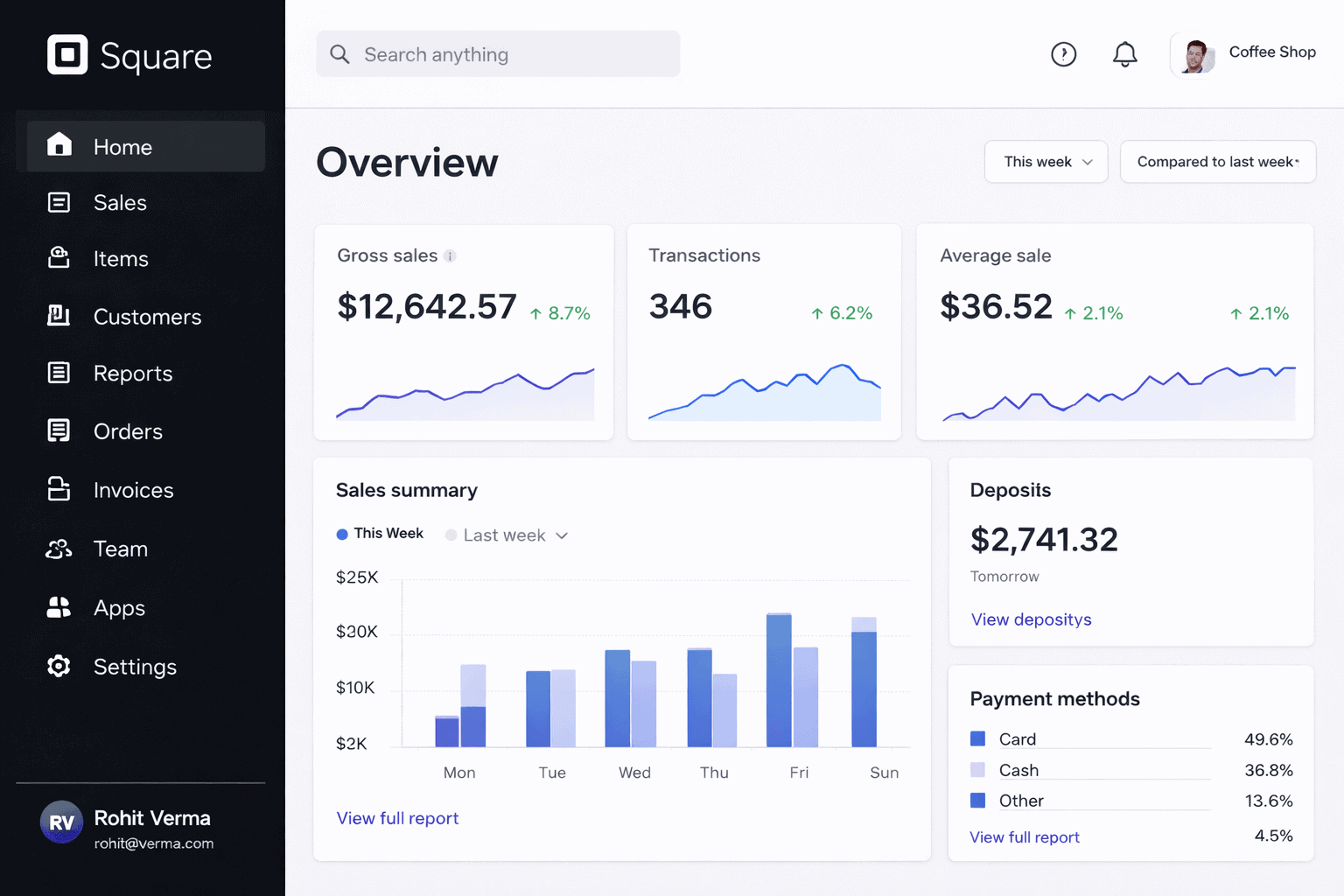

2. Square

Square is an all-in-one commerce ecosystem that started with in-person payments and expanded online. It bundles a payment gateway, point-of-sale software, an online store builder, and business tools, all designed to work without a developer. For retailers, restaurants, and service businesses that sell both in person and online, Square is the natural Stripe alternative.

Pros

- Omnichannel by default: in-person, online, and invoice payments live in one ecosystem.

- Fast setup: no approval process and a free POS app included.

- No monthly fee to start: the free plan covers standard processing.

- Cheaper in person: in-person rates beat Stripe’s card-present pricing.

Cons

- Weak for subscriptions: recurring billing is basic, fine for a gym membership, frustrating for complex SaaS pricing.

- Limited global reach: available in only about nine countries, so it’s a poor fit for global expansion.

- Account holds: reviewers report occasional random holds and slow support during disputes.

Pricing

Square charges 2.9% + $0.30 for online payments and 2.6% + $0.15 for in-person transactions on the free plan. Paid plans (Plus at $49/month, Premium at $149/month per location) lower in-person rates. Check detailed pricing here.

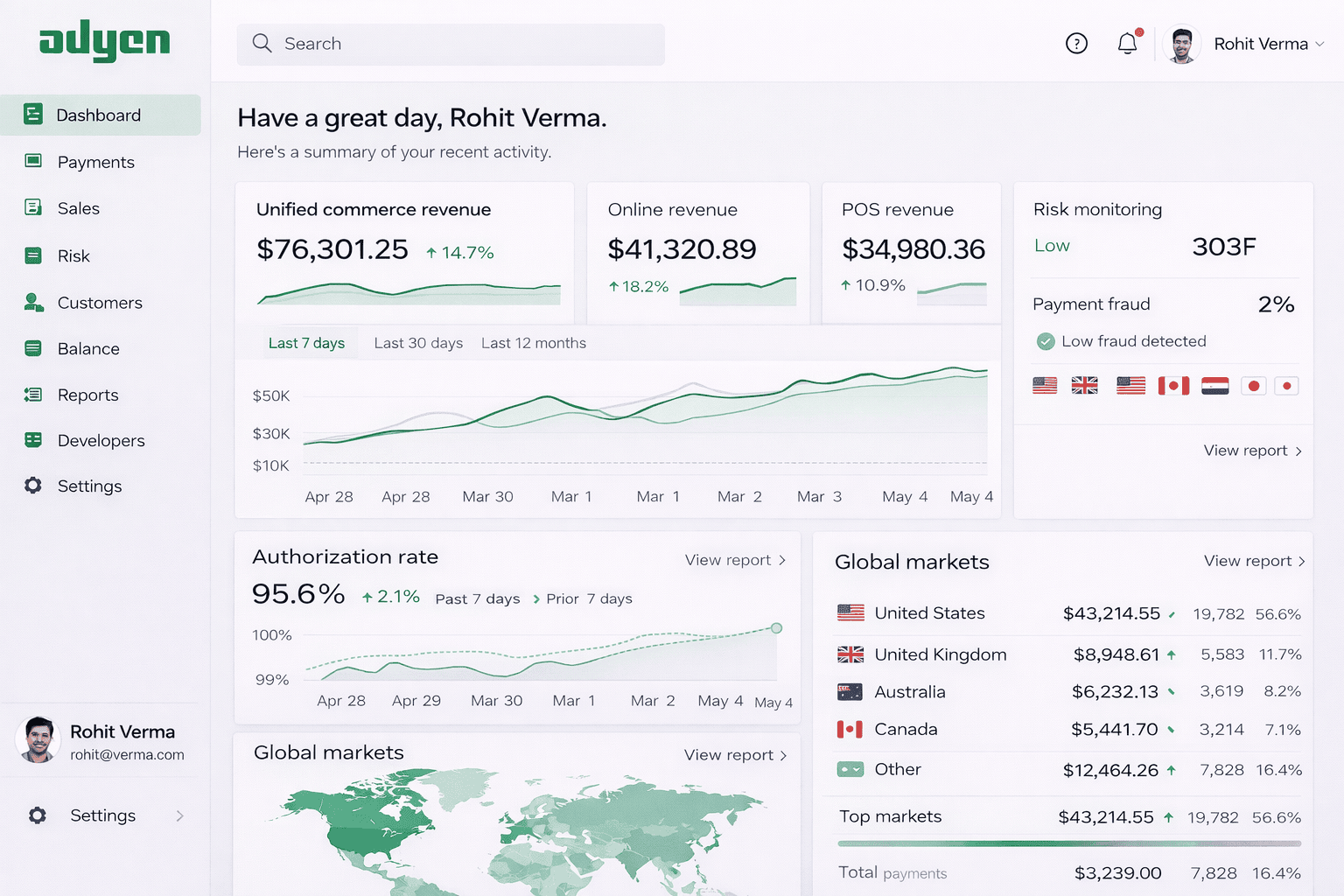

3. Adyen

Adyen is an enterprise-grade payment platform built for global scale. It’s the processor behind brands like Uber, Spotify, and eBay, offering acquiring, gateway, and omnichannel capabilities in one system with direct connections to card networks. For high-volume businesses selling internationally, Adyen’s interchange-plus pricing often works out cheaper than Stripe’s flat rate.

Pros

- Cheaper at scale: for businesses processing $500K+/month, Adyen averages 2.4-2.8% total versus Stripe’s flat 2.9% + $0.30.

- Transparent pricing: the Interchange++ model itemizes exactly what card networks and Adyen charge.

- Global infrastructure: 150+ currencies and direct acquiring across regions.

- Unified platform: online, mobile, and in-store payments in one place, with 24/7 support included.

Cons

- Monthly minimum prices out small merchants: a minimum invoice of roughly $120/month means low-volume businesses pay the difference.

- Complex setup: integration is technical and onboarding involves strict KYC checks.

- Conservative risk appetite: Adyen frequently declines high-risk industries.

Pricing

Adyen uses Interchange++ pricing: interchange plus card-scheme fees plus a markup of around 0.6%, with a base fee near $0.13 per transaction. Expect a monthly minimum of roughly $120. Check detailed pricing here.

4. Braintree

Owned by PayPal, Braintree offers similar trust and recognition while adding advanced features like customizable checkout. It supports a wide range of payment methods and prioritizes security with advanced fraud detection. The PayPal ownership means native PayPal acceptance, something Stripe can’t offer.

Pros

- Competitive fees: attractive rates, particularly for high transaction volumes.

- Flexibility: supports many payment methods plus customizable checkout, including native PayPal and Venmo.

- Security: robust fraud detection built in.

- Global reach: operates across 45+ countries.

Cons

- International fees: higher fees on cross-border transactions.

- Limited platform support: integration options are thinner for some ecommerce platforms.

- Setup effort: some advanced features need extra configuration.

Pricing

Braintree charges 2.59% + $0.49 per transaction, with fees varying by volume and currency. Check detailed pricing here.

5. Authorize.net

Authorize.net is one of the original payment gateways, known for rock-solid reliability and a vast ecosystem of plugins. If an app accepts payments, it probably supports Authorize.net. It integrates with countless ecommerce platforms and includes an Advanced Fraud Detection Suite to safeguard transactions.

Pros

- Reliability: highly predictable, with a huge ecosystem of plugins and partners.

- Flexibility: supports many payment methods and integrates almost everywhere.

- Security: tokenization and a built-in fraud detection suite.

- Established: a trusted, battle-tested gateway for older and legacy systems.

Cons

- Monthly gateway fee: the $25/month adds up alongside merchant account fees.

- Dated experience: the API and interface feel older than modern platforms like Stripe.

- Separate merchant account: can add setup complexity.

Pricing

Authorize.net charges 2.9% + $0.30 per transaction plus a $25 monthly gateway fee. Check detailed pricing here.

6. Razorpay

Razorpay is built for businesses operating in India and Southeast Asia. It supports local payment methods like UPI, net banking, and wallets, with GST-friendly invoicing and a developer experience tailored to Indian businesses. For the Indian market, it’s often the strongest option on this list.

Pros

- Low domestic fees: a flat 2% on most domestic transactions undercuts global gateways.

- Local methods: deep support for UPI, net banking, and wallets.

- No setup or maintenance fees: pure pay-as-you-go with high success rates.

- Full stack: adds banking, payroll, and lending through RazorpayX and Capital.

Cons

- Limited geographic coverage: built for India, less useful for global businesses.

- GST on fees: 18% GST applies on top of the 2%, making the effective rate around 2.36%.

- Technical setup: customizations require developer involvement.

Pricing

Razorpay charges a flat 2% on domestic transactions plus 18% GST, and around 3% on international cards. There are no setup or annual maintenance fees. Check detailed pricing here.

For businesses using Razorpay, dedicated Razorpay analytics tools can provide deeper insight into payment performance.

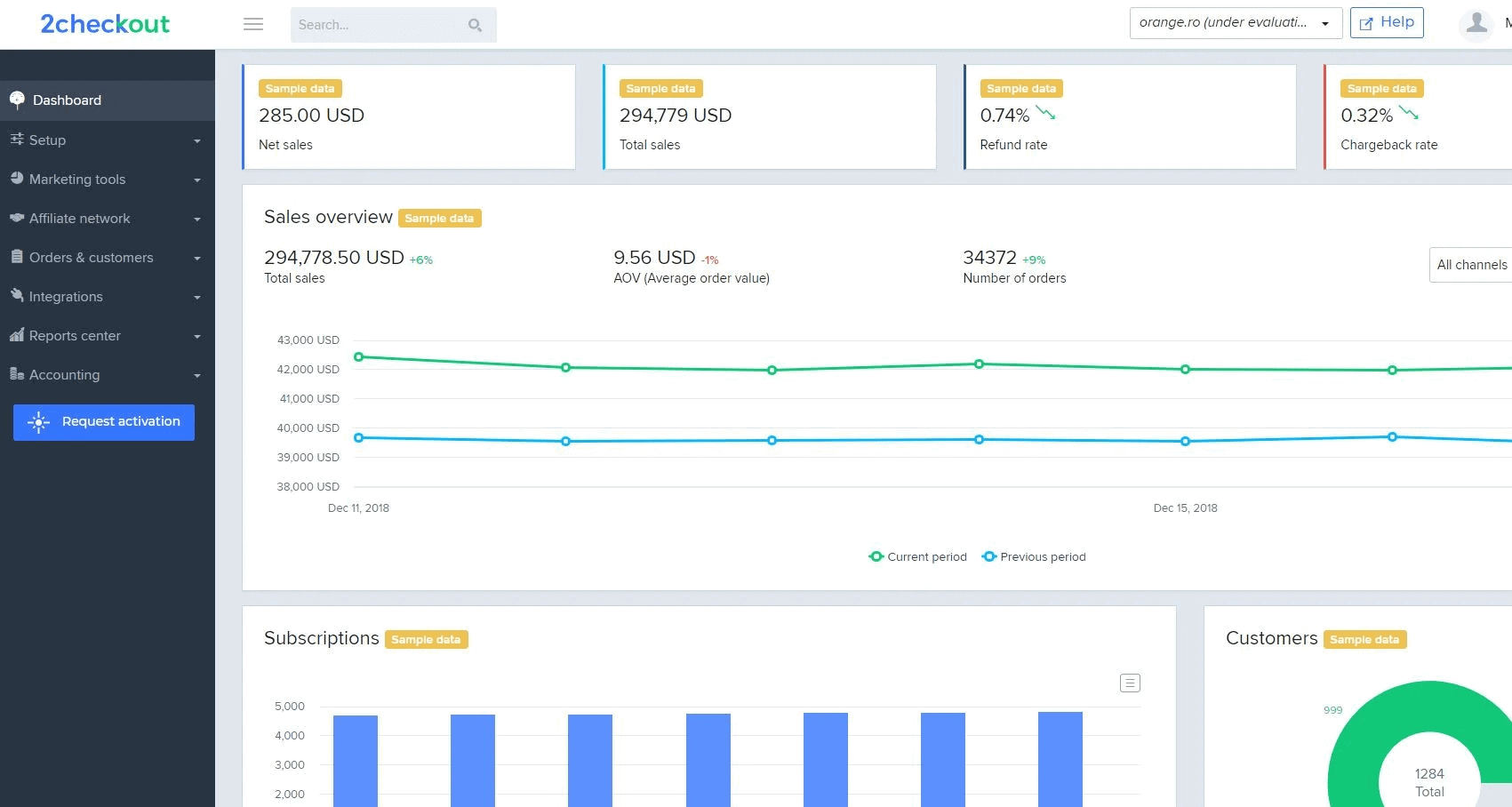

7. 2Checkout (Verifone)

2Checkout, now part of Verifone, is a global monetization platform for SaaS companies, digital product sellers, and ecommerce businesses. It supports multiple currencies and payment methods, and unlike a plain gateway, it can act as a merchant of record that handles tax, compliance, and invoicing for you.

Pros

- Global selling: supports many currencies and local payment methods worldwide.

- Merchant-of-record option: can handle taxes, compliance, and local laws on your behalf.

- Subscription tools: built-in recurring billing, dunning, and revenue recovery.

- Security: tokenization and PCI compliance.

Cons

- Higher fees: rates climb from 3.5% to 6% depending on the plan you choose.

- Approval friction: reviewers report inconsistent application approvals.

- Limited customization: checkout flexibility is narrower than Stripe’s.

Pricing

2Checkout uses tiered pricing: 2Sell at 3.5% + €0.30, 2Subscribe at 4.5% + €0.40, and 2Monetize (full merchant of record) at 6.0% + €0.50 per sale. Check detailed pricing here.

8. Paddle

Paddle is a merchant-of-record platform built specifically for SaaS and software companies. Instead of acting as a payment gateway you bolt tax tools onto, Paddle becomes the legal seller. It handles payment processing, global sales tax and VAT, fraud screening, and chargebacks under one roof, so you can sell worldwide without registering for tax in every jurisdiction.

Pros

- Tax handled for you: Paddle remits VAT, GST, and sales tax across 200+ jurisdictions.

- One bundled fee: payments, tax, invoicing, and subscriptions in a single rate.

- Built-in analytics: includes ProfitWell subscription analytics at no extra cost.

- Chargebacks covered: as merchant of record, Paddle fights disputes for you.

Cons

- Higher headline rate: 5% + $0.50 is well above Stripe’s 2.9% + $0.30.

- Currency conversion margins: FX spreads can push the effective rate to 7-8% on international sales.

- Brand on receipts: Paddle appears as the seller on customer statements, which can confuse buyers.

Pricing

Paddle charges 5% + $0.50 per transaction with no monthly fee on the standard plan. Currency conversion margins apply on international sales. Check detailed pricing here.

How do these alternatives handle subscription billing?

If you run a SaaS or subscription business, payment processing is only half the job. You also need solid recurring billing. Here’s how each platform handles subscriptions in 2026.

Stripe: the gold standard for subscription management. Stripe Billing supports 15+ pricing models natively, including flat-rate, tiered, per-unit, volume-based, and usage-based billing, with built-in dunning to recover failed payments.

PayPal: handles simple monthly or annual plans through subscription buttons and billing agreements. For complex pricing or usage-based billing, you’ll likely need a third-party tool.

Square: recurring features are functional but basic. Fine for a fixed membership, limiting for SaaS with sophisticated or usage-based pricing.

Adyen: supports recurring payments and tokenized billing at enterprise scale, but it expects you to bring your own subscription logic rather than offering a turnkey billing suite.

Braintree: handles basic subscription scenarios well, with plans, trials, and discounts. The catch is that it can’t easily change billing frequency on existing plans, and there’s no native usage-based billing.

Authorize.net: Automated Recurring Billing handles fixed-interval charges reliably, but it lacks the flexibility of Stripe for complex tiers or mid-cycle changes.

Razorpay: Razorpay Subscriptions supports recurring payments with automatic retries and UPI-based mandates, strong for the Indian market, more limited globally. A 0.99% subscription fee applies on top of the gateway rate.

2Checkout (Verifone): built for digital products and global subscriptions, with subscription management, automated tax handling, and churn-reduction tools through its 2Subscribe plan.

Paddle: full subscription billing with trials, discounts, plan changes, and dunning, all wrapped inside the merchant-of-record model, so tax on each renewal is handled automatically.

The bottom line: if subscription billing is core to your business, Stripe offers the most flexibility. But if your needs are simpler or region-specific, Razorpay (for India) or a merchant of record like Paddle or 2Checkout (for global digital products) can be the better fit.

What’s the best Stripe alternative?

Each alternative has its own strengths, which means there’s no single best Stripe alternative. The right choice depends on where you sell, what you sell, and who your customers are.

In fact, many businesses end up using more than one. Here’s why that’s common:

- Redundancy: running two gateways keeps payments flowing if one has downtime or a technical issue.

- Geography: one gateway for domestic transactions, another for international.

- Multiple stores: businesses running several brands or models often use different gateways for each.

There’s real data behind this. According to McKinsey’s Digital Payments research, multi-gateway routing reduces payment failures by 25% and improves authorization rates by 5-10%. Using more than one processor isn’t just a safety net. It can directly recover revenue.

But juggling several payment platforms creates a new problem: your data is scattered across multiple dashboards. That’s where Putler comes in.

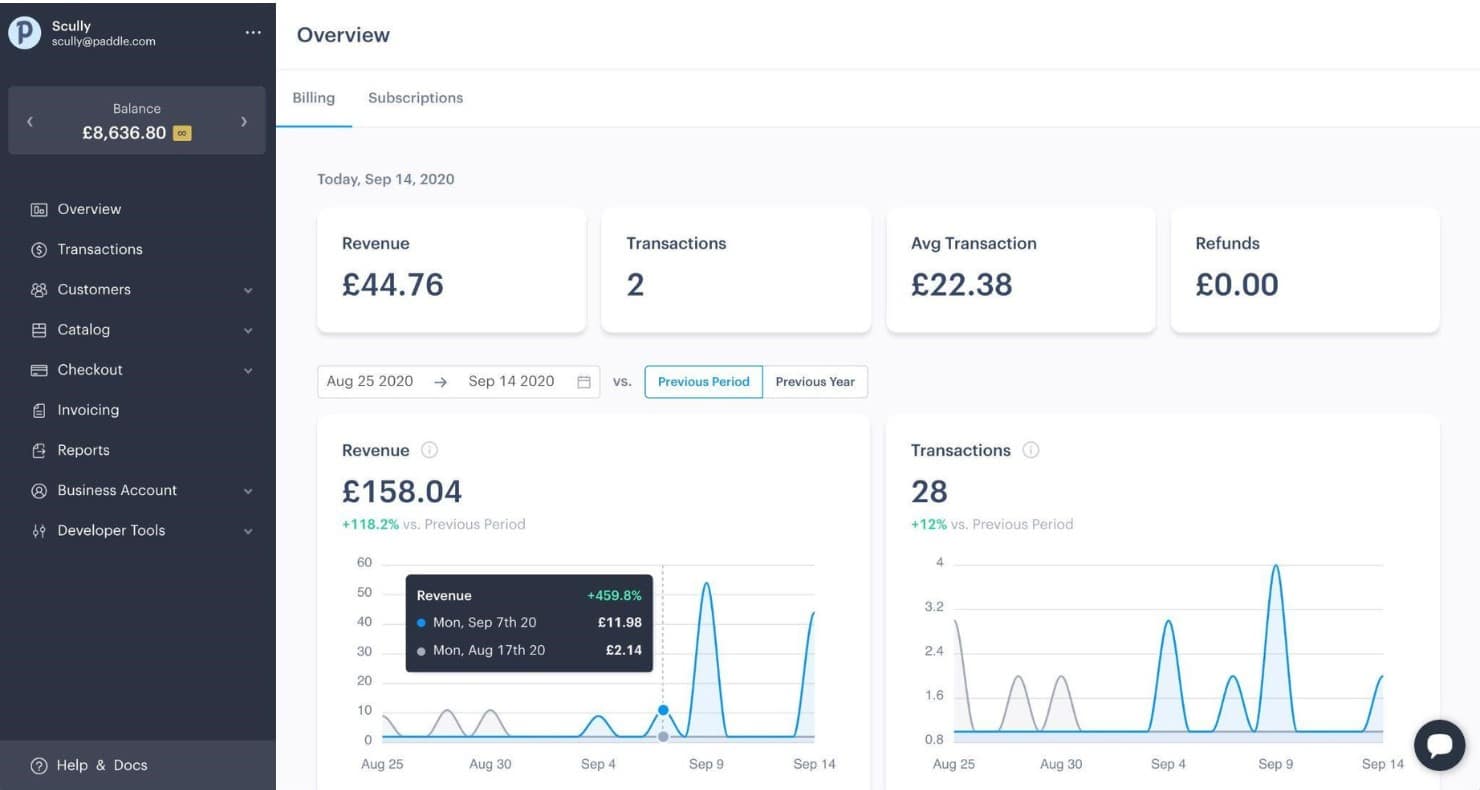

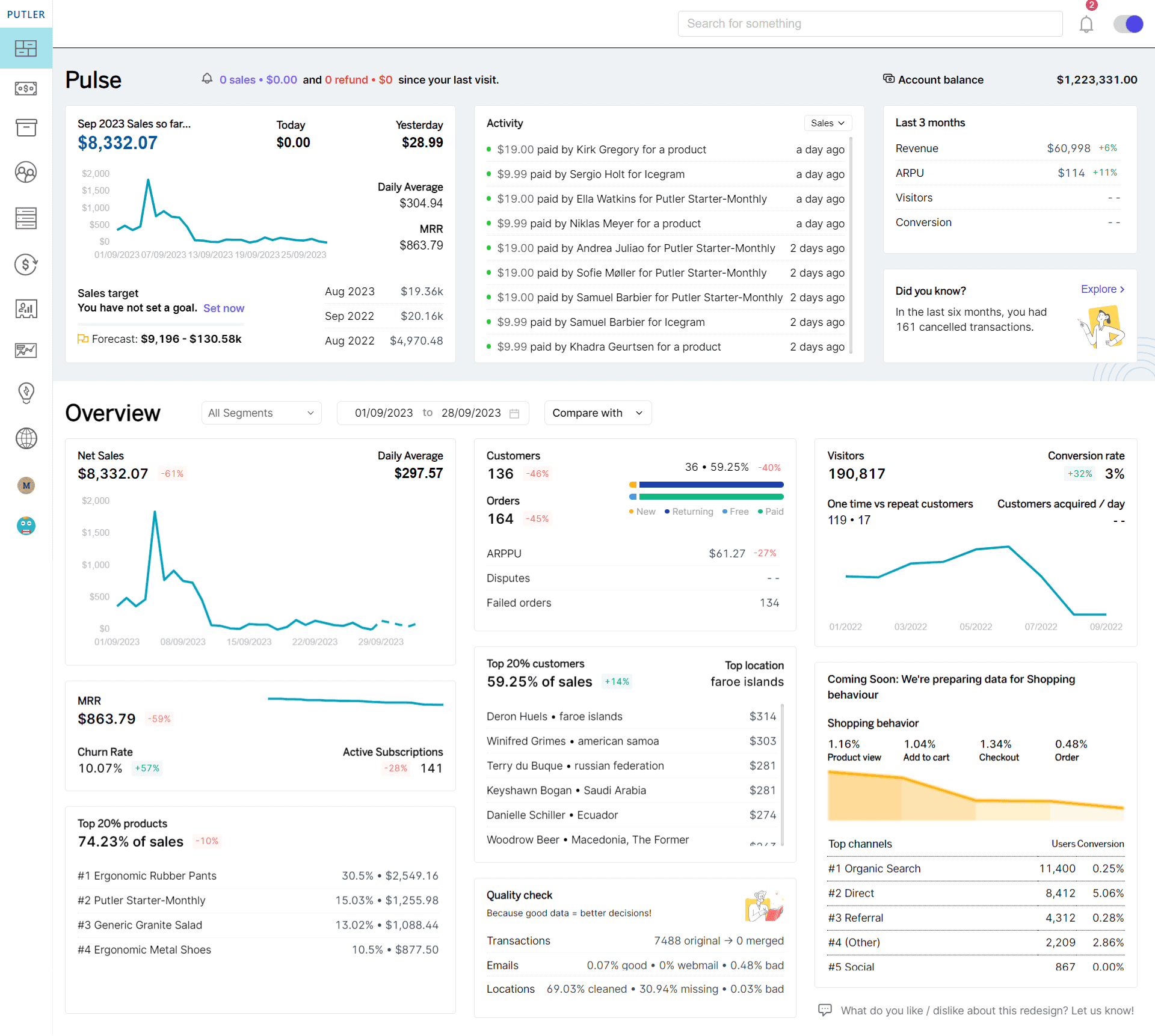

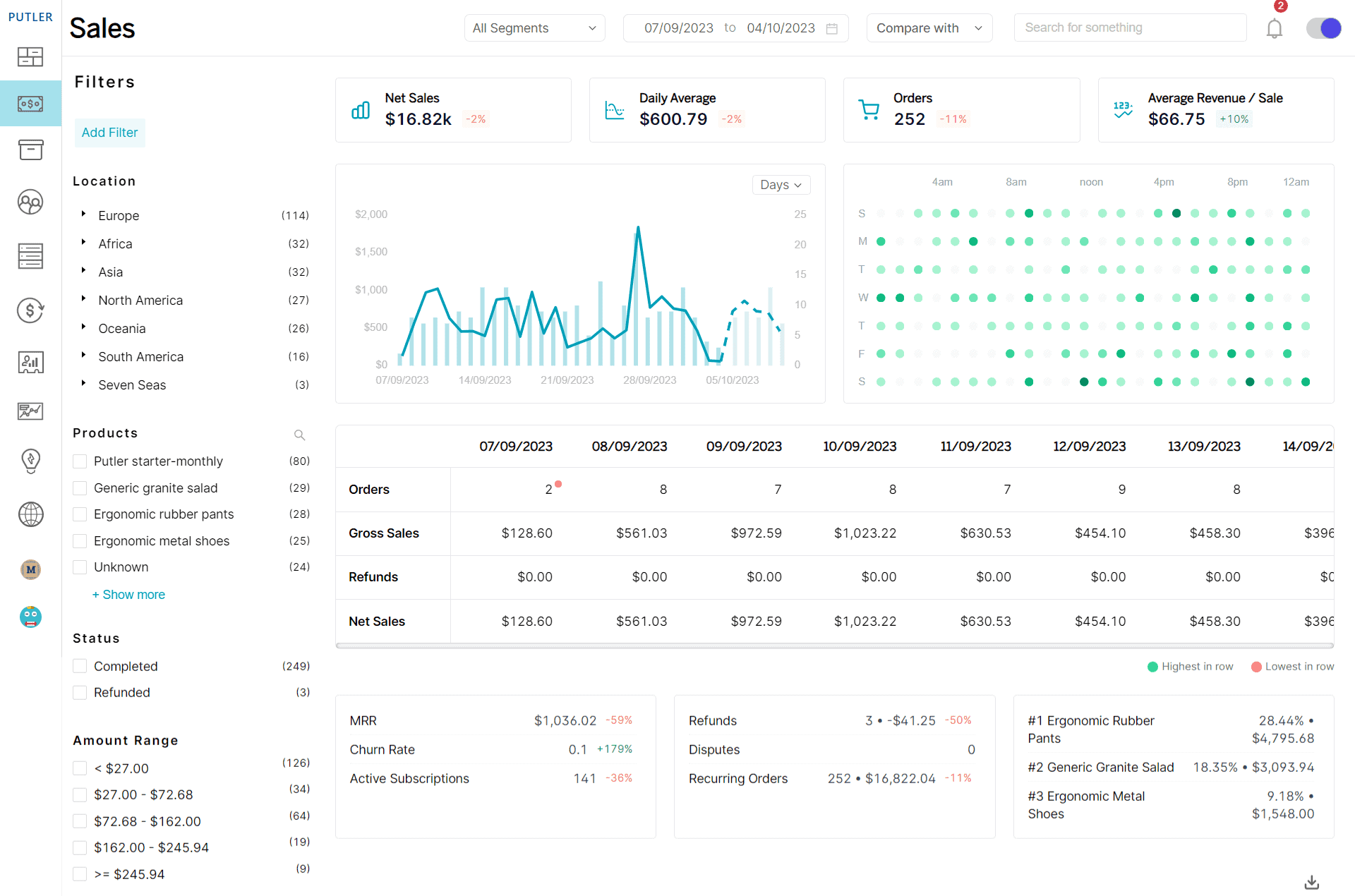

Putler: all payment gateways in a single dashboard

Putler is not a payment gateway and not a Stripe alternative in the processing sense. It’s the layer above them. Putler connects all the gateways covered in this article into one dashboard, so payment management stops being a tab-switching exercise.

If you’re tired of logging into several platforms to piece together your numbers, Putler brings them together and cleans the data before showing it to you.

One unified dashboard

Putler consolidates data from 7+ payment gateways, including Stripe, PayPal, Authorize.net, Braintree, 2Checkout, and Razorpay, into one place. It aggregates, deduplicates, and enriches the data before presenting it, so you no longer log into multiple platforms or stitch together spreadsheets to see your real numbers.

Real-time insights

Putler gives you up-to-the-minute insight into sales performance, refund rates, and customer behavior across every connected gateway. You can monitor transactions as they happen and respond quickly to changes.

Advanced analytics

Beyond basic reporting, Putler digs into trends, patterns, and customer lifetime value. With Stripe payment analytics and support for other gateways, you get a complete picture of business performance across all your payment sources, not one platform at a time.

Direct refunds

Putler reduces the refund process to two steps, removing the multi-step hassle of logging into each platform. It currently supports direct refunds for Stripe, PayPal, Braintree, and Shopify.

One workflow

With everything consolidated, there’s no more tab-switching or exporting CSVs to reconcile your data. Putler handles the consolidation so you can focus on growing the business instead of assembling reports.

Choosing the right Stripe alternative

The best Stripe alternative is the one that fits how your business actually runs. Square suits in-person and omnichannel retail. Adyen fits high-volume global enterprises. Razorpay wins in India. Paddle and 2Checkout handle tax for global SaaS. PayPal and Braintree bring consumer trust.

Most growing businesses will run more than one of these before long. When that happens, the smart move is to stop checking each dashboard separately and consolidate your reporting in one place.

FAQs about Stripe alternatives

What is the best Stripe alternative?

There’s no single best Stripe alternative, because the right one depends on your business. PayPal and Braintree win on consumer trust, Square on in-person retail, Adyen on enterprise global volume, Razorpay in India, and Paddle or 2Checkout for global SaaS that wants tax handled through a merchant of record.

Who is Stripe’s biggest competitor?

PayPal is Stripe’s biggest competitor. Both offer online payment processing and developer-friendly APIs, though PayPal adds far wider consumer recognition. Other major competitors include Square, Adyen, and Braintree.

Is Stripe the best option for selling SaaS?

Stripe is excellent for SaaS thanks to its flexible billing and developer-friendly APIs. But it isn’t a merchant of record, so you stay responsible for global tax. SaaS companies selling worldwide often prefer Paddle or 2Checkout, which handle tax and compliance for you.

Are there cheaper alternatives to Stripe?

Yes. For high-volume businesses, interchange-plus processors like Adyen and Helcim often beat Stripe’s flat 2.9% + $0.30. In India, Razorpay’s 2% domestic rate is lower. The cheapest option depends on your volume, location, and card mix.

Who is better, Stripe or PayPal?

It depends on your priorities. Stripe offers customizable checkout, lower per-transaction fees, and a better developer experience. PayPal offers more payment methods, stronger consumer trust, and wider global reach. Many businesses use both.